Archiving Requirements for Accounting in Austria

Veröffentlicht am 21.05.2026

Lesedauer: 8 min

Contents

- What Does the Retention Obligation in Accounting Mean?

- An Overview of Retention Periods for Accounting Records

- Which Documents Must be Retained?

- Storing Documents: Paper or Digital?

- Common Mistakes in Document Retention and How to Avoid Them

- Efficiently Meet Accounting Retention Requirements with free-com

- Frequently Asked Questions About the Requirement to Retain Receipts

Inhalt

- What Does the Retention Obligation in Accounting Mean?

- An Overview of Retention Periods for Accounting Records

- Which Documents Must be Retained?

- Storing Documents: Paper or Digital?

- Common Mistakes in Document Retention and How to Avoid Them

- Efficiently Meet Accounting Retention Requirements with free-com

- Frequently Asked Questions About the Requirement to Retain Receipts

Austrian companies are legally required to retain books, records, and supporting documents for a specified period of time. The relevant retention periods, types of documents affected, and formal requirements are governed by the Federal Tax Code (BAO) and the Commercial Code (UGB).

This article provides a structured overview of the applicable retention periods in accounting. It also identifies which documents are affected and explains how to properly fulfill the retention obligation toward the tax authorities—including in the context of digital archiving.

What Does the Retention Obligation in Accounting Mean?

The retention obligation requires Austrian companies to keep accounting documents and receipts complete, organized, and available for audit at any time for a minimum period specified by law.

Legal Basis in Austria

The requirement to retain accounting records in Austria is enshrined in two key laws: the Federal Tax Code (BAO) and the Commercial Code (UGB).

The BAO (Section 132) governs the tax-related retention requirement and applies to all taxpayers, regardless of legal form or company size. The UGB (Section 212) supplements this with commercial law requirements for companies subject to accounting obligations. Both sets of regulations stipulate that books, records, and supporting documents must be retained in such a way that they are traceable and verifiable at all times.

Who is subject to the record-keeping requirement?

In general, the record-keeping requirement applies to the accounting records of all business entities in Austria, including:

- Corporations (GmbH, AG)

- Partnerships (OG, KG)

- Sole proprietors and self-employed professionals

- Associations and non-profit organizations engaged in business activities

Even if a business does not maintain a full double-entry bookkeeping system but instead uses a cash basis accounting system, the retention requirement applies to all relevant documents and records.

An Overview of Retention Periods for Accounting Records

Different retention periods apply in Austria depending on the type of document. These range from 7 to 22 years, although the start of the retention period is uniformly regulated.

The 7-Year Period as the Standard Rule

The standard retention period for accounting records in Austria is 7 years. This applies to the vast majority of all accounting documents: invoices, bank statements, contracts, cash reports, and other tax-relevant documents must be retained for at least 7 years.

Special 10-Year Retention Period

In addition to the standard 7-year period, the following areas are subject to a special retention period of 10 years:

- Electronic Services & OSS: Documents related to electronically provided services, telecommunications, radio, and television services provided to non-business entities in EU member states and for which the One-Stop-Shop (OSS) is used must be retained for 10 years.

- Platform Liability: Records from platforms related to platform liability are also subject to the 10-year retention period.

- COVID-19 Subsidies: Different retention periods apply here depending on the type of subsidy:

| Covid-19 Subsidies | Retention Period |

|---|---|

| Investitionsprämie | 10 Years |

| Kurzarbeitsbeihilfe | 10 Years |

| Härtefallfonds (Phase 1) | 10 Years |

| Härtefallfonds (übrige Phasen) | 7 Years |

| Fixkostenzuschuss I & 800.000 | 7 Years |

| Ausfallsbonus I, II & III | 7 Years |

| Verlustersatz | 7 Years |

When Does the 22-year Period Apply?

Significantly longer retention periods apply to certain documents. The 22-year period is particularly relevant for land and real estate transactions. This is due to input tax credits related to real estate: Since these can be adjusted for up to 20 years, the corresponding supporting documents must be retained for that length of time.

This includes, for example, purchase agreements, invoices for construction and renovation work, as well as all other documents related to the acquisition or construction of buildings and land.

When Does the Retention Period Begin?

The retention period does not start on the date of the document, but at the end of the fiscal year in which the underlying transaction took place. A document from March 2020 must therefore be retained until at least December 31, 2027. In the case of ongoing contracts or legal disputes, the retention requirement is extended until the conclusion of the respective matter.

Which Documents Must be Retained?

The retention requirement covers all documents necessary for tracing business activities and verifying a company’s tax situation.

Accounting Records & Financial Statements

The core of the documents subject to retention requirements includes all documents that form the basis of your accounting: financial statements and balance sheets, income statements, cash books, general ledgers, and all accounting records that allow business transactions to be traced.

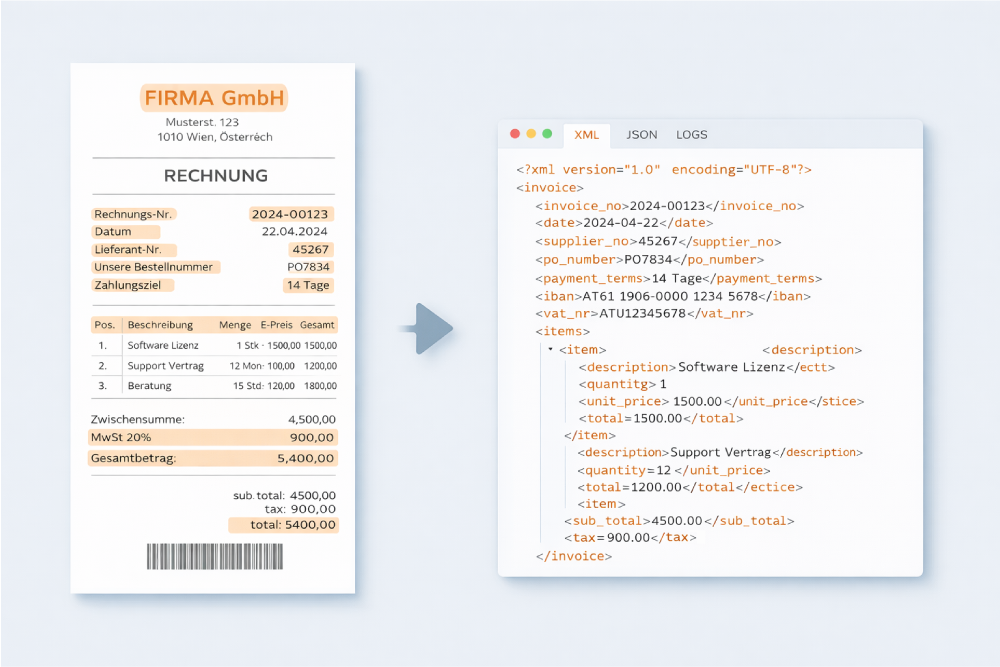

Incoming and Outgoing Invoices

nvoices are the cornerstone of document retention. Both incoming and outgoing invoices must be retained in their entirety and in a legible condition. Special requirements apply to the content of invoices, as only properly documented invoices qualify for input tax deduction.

Important: Thermal paper receipts fade over time and must therefore always be copied or digitized before they become illegible.

Contracts, Payroll Records and Other Documents

The following documents are also subject to the retention requirement:

- Employment contracts and payroll records (pay stubs, employment contracts, time sheets)

- Supply contracts, rental and lease agreements with tax relevance

- Bank statements, transfer confirmations, and account statements

- Business emails and correspondence with tax implications

- Customs documents and proof of import for international transactions

Storing Documents: Paper or Digital?

The decision between paper and digital storage has far-reaching practical implications. Both options are permitted in Austria, provided that legal requirements are met.

Paper Storage: Requirements and Limitations

Traditional paper-based storage is still fully recognized in Austria. Companies that physically archive their documents must adhere to the following principles:

- Organized filing: Documents must be organized systematically and in a traceable manner, for example by date, document type, or business transaction, so that an audit can be conducted without disproportionate effort.

- Completeness: No document may be missing. Gaps in the document chain can lead to estimates during a tax audit.

- Legibility: Documents must remain legible throughout the entire retention period. Thermal paper receipts pose a well-known problem here, as they fade within a few years. They should therefore always be copied.

- Protection against damage: Paper documents must be protected from moisture, light, and other damaging influences. Water damage or fire can destroy the entire archive.

- Accessibility: The documents must be available for presentation promptly in the event of an audit.

The main drawbacks of paper-based record-keeping are obvious: it takes up a lot of space, requires manual searching, lacks redundancy in case of loss, and has limited accessibility. This is particularly true for distributed teams or multiple locations.

Digital Storage of Documents in Austria

In Austria, the digital archiving of accounting documents is generally permitted and recognized by the tax authorities—provided certain requirements are met. The documents must be stored completely, accurately, in a timely manner, and in an organized fashion. Additionally, they must be viewable at all times.

Particularly important: The documents must be stored in a file format that remains readable over the long term. PDF/A is the standard and recommended format for long-term archiving.

Compared to traditional paper archiving, the digital storage of documents offers significant advantages:

Common Mistakes in Document Retention and How to Avoid Them

Even well-organized companies make typical mistakes when it comes to document retention—often because they are unaware of the exact legal requirements.

Efficiently Meet Accounting Retention Requirements with free-com

The legal requirements for document retention are complex, but the technical implementation does not have to be. free-com offers solutions that step in exactly where manual processes reach their limits. Automated invoice processing, audit-proof archiving, automatic document recognition, and seamless system integration ensure that you meet your legal obligations without any additional effort.

Do You Have Any Questions For Us?

We will be happy to consult you during a short, non-binding online appointment!