Mandatory E-Invoicing in Germany: What Businesses Need to Know

Veröffentlicht am 25.06.2026

Lesedauer: 5 min

Contents

Inhalt

Since January 1, 2025, mandatory e-invoicing has applied to the B2B sector in Germany. All companies based in Germany that conduct business with other companies based in Germany must be able to issue and receive electronic invoices. A PDF invoice sent by email is no longer considered an e-invoice within the meaning of the law.

Germany is therefore following the EU strategy to prevent VAT fraud and to make invoice processing simpler and more sustainable. So it is high time to review your own processes and take the right steps.

Who Is Affected by Mandatory E-Invoicing?

Mandatory e-invoicing applies to all taxable B2B transactions between companies based in Germany, regardless of size or revenue. It affects companies with their registered office, management, or a permanent establishment involved in the respective transaction in Germany. If there is no registered office, place of residence or habitual residence in Germany also counts as a criterion.

Small businesses are also affected, at least when it comes to receiving e-invoices. The ability to receive electronic invoices is mandatory for all companies, with no transitional arrangement.

Transactions that are VAT-exempt under Section 4 nos. 8 to 29 UStG, as well as invoices issued to private individuals (B2C), are not covered by mandatory e-invoicing.

What Is an E-Invoice and What Is Not?

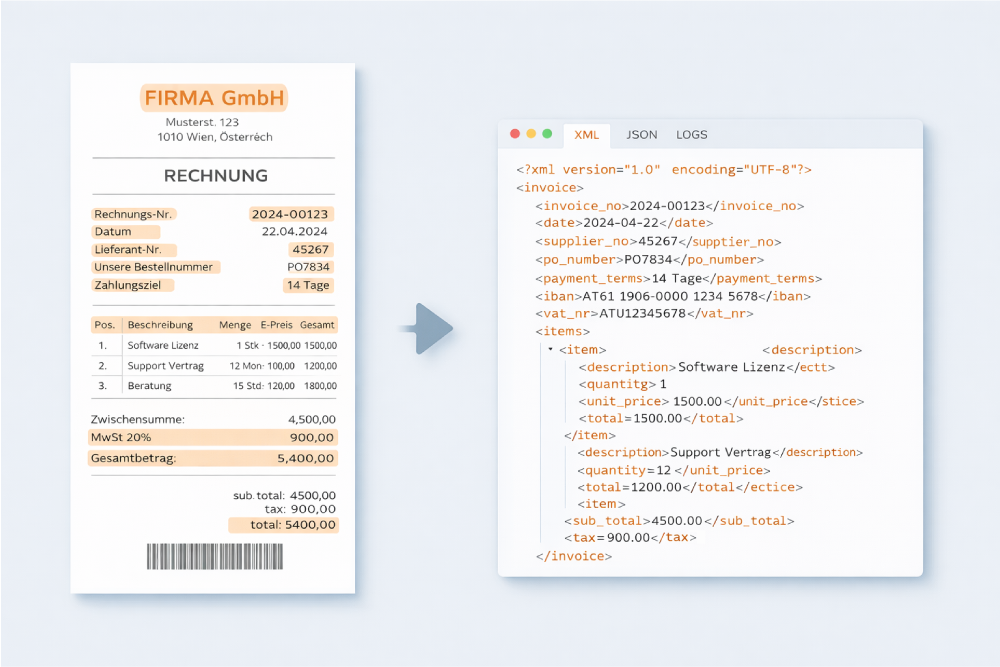

An e-invoice is not simply an invoice that is sent digitally. It must be created, transmitted, and received in a structured e-invoicing format so that the data record can be processed automatically. The basis is the European standard EN 16931.

In addition, e-invoices must meet the same tax law requirements as paper invoices: from the authenticity of origin and the integrity of content through to readability. We have summarized in detail which specific mandatory information an e-invoice must contain and which organizational prerequisites your company must meet: Electronic Invoice: Requirements and Prerequisites.

A PDF invoice sent by email has no longer been considered an e-invoice since January 1, 2025. PDF invoices and paper invoices are classified as “other invoices” and are no longer permitted in the B2B sector, with the exception of the applicable transitional arrangements.

The Phases of Mandatory E-Invoicing

Full mandatory e-invoicing is being introduced for companies in stages. There is no transitional period for receiving e-invoices. This has had to be possible since January 1, 2025. The following stages apply to issuing invoices:

| Time Period | What Applies? |

|---|---|

| From January 1, 2025 | Receiving e-invoices: mandatory for all companies. Issuing invoices: transitional arrangements apply. |

| Until December 31, 2026 | Other invoices (e.g. PDF) may still be issued if the recipient agrees. |

| Until December 31, 2027 | Other invoices only for companies with prior-year revenue of max. €800,000 (2026). EDI invoices remain permitted with consent. |

| From January 1, 2028 | Full mandatory e-invoicing for all companies, no exceptions. |

Important: The relevant point in time for the transitional arrangements is the time the invoice is transmitted, not the performance date.

Benefits of Mandatory E-Invoicing for Companies

Mandatory e-invoicing initially requires investment, but it pays off quickly:

- Faster Processes, Fewer Errors: Structured data can be fed directly into existing systems. Manual entry, typing errors, and media breaks are eliminated. Processing times are noticeably reduced, and cash discount deadlines are met more reliably.

- More Efficient Use of Resources: By eliminating manual processing steps, your employees can focus on value-adding tasks.

- Sustainability: No paper, no physical dispatch, no physical archiving. Approval processes run fully digitally, regardless of location and with full flexibility.

- Future Readiness: Companies that switch now are not only legally compliant, but also prepare their business for further digitalization steps. For example, automated invoice processing or digital archiving.

What Do Companies Specifically Need to Do?

Mandatory e-invoicing affects companies on two levels: inbound and outbound invoices. Here are the most important immediate measures:

- 1

- 2

Choose an E-Invoicing Format

Decide which format you will use for digital outbound invoices in the future. For many SMEs, ZUGFeRD offers the advantage that the invoice is both machine-readable and presented as a PDF for humans.

- 3

Adapt Systems and Processes

Make sure that your software can not only receive e-invoices, but also archive them correctly. Since 2025, the retention period has been at least eight years.

- 4

Know and Use Transitional Periods

If you have not yet fully switched over, check which transitional period applies to your company and plan the changeover accordingly. From 2028, there will be no more exceptions.

Meet Mandatory E-Invoicing Requirements With free-com

Mandatory e-invoicing is no longer a distant requirement, but a lived reality. With the right solution, however, the switch can be implemented smoothly while making the entire invoice process more efficient at the same time.

As experts in digital invoice processing, free-com supports you in receiving and automatically processing all common e-invoicing formats, in digital approval processes with a complete audit trail, and in audit-proof archiving. Flexible for different company sizes and system environments.

Do You Have Any Questions For Us?

We will be happy to consult you during a short, non-binding online appointment!