Electronic Invoicing: Requirements and Prerequisites

Veröffentlicht am 30.03.2026

Lesedauer: 10 min

Contents

- E-Invoice, PDF Invoice & Paper Invoice – These are the Differences

- Optimizing Costs and Workload Through E-Invoicing

- Formats for the E-Invoice

- The Most Important Legal and Organizational Requirements for Electronic Invoicing

- What Mandatory Information is Required for an E-Invoice?

- Introducing Electronic Invoicing: Step by Step

- E-Invoice Checklist: Some Questions You Should Ask Yourself During the Transition

- Conclusion: Implement E-Invoicing Requirements Early On

- Frequently Asked Questions About Electronic Invoices

Inhalt

- E-Invoice, PDF Invoice & Paper Invoice – These are the Differences

- Optimizing Costs and Workload Through E-Invoicing

- Formats for the E-Invoice

- The Most Important Legal and Organizational Requirements for Electronic Invoicing

- What Mandatory Information is Required for an E-Invoice?

- Introducing Electronic Invoicing: Step by Step

- E-Invoice Checklist: Some Questions You Should Ask Yourself During the Transition

- Conclusion: Implement E-Invoicing Requirements Early On

- Frequently Asked Questions About Electronic Invoices

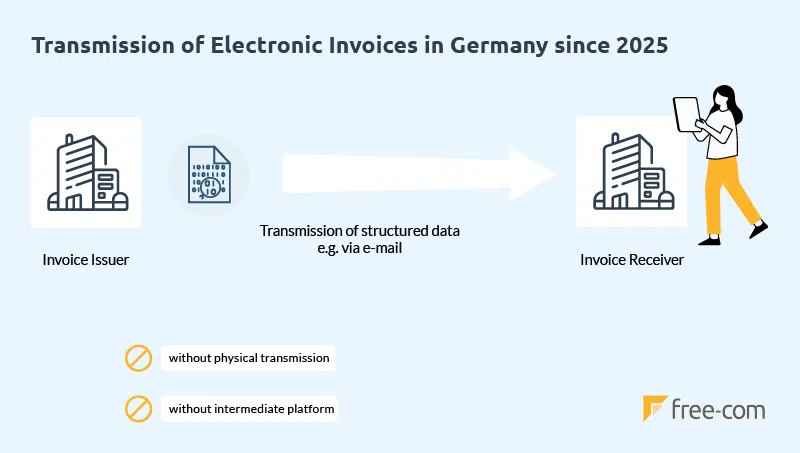

Since 2020, all federal government suppliers in Germany have been required to use electronic invoicing. On January 1, 2025, this requirement was also extended to the B2B sector as part of the Growth Opportunities Act.

Using e-invoices offers not only financial benefits but also the opportunity to optimize and automate your financial accounting. However, there are several requirements to consider when switching to electronic invoicing. We have summarized these for you here.

E-Invoice, PDF Invoice & Paper Invoice – These are the Differences

The definition of an e-invoice often leads to confusion. This is probably due to the fact that, according to Section 14 of the German Value Added Tax Act (UStG), any invoice that is issued and received electronically is an electronic invoice. According to tax law, a simple PDF invoice that you send to your service recipients by email is therefore also considered an electronic invoice. However, this definition does not comply with the new guidelines that took effect on January 1, 2025.

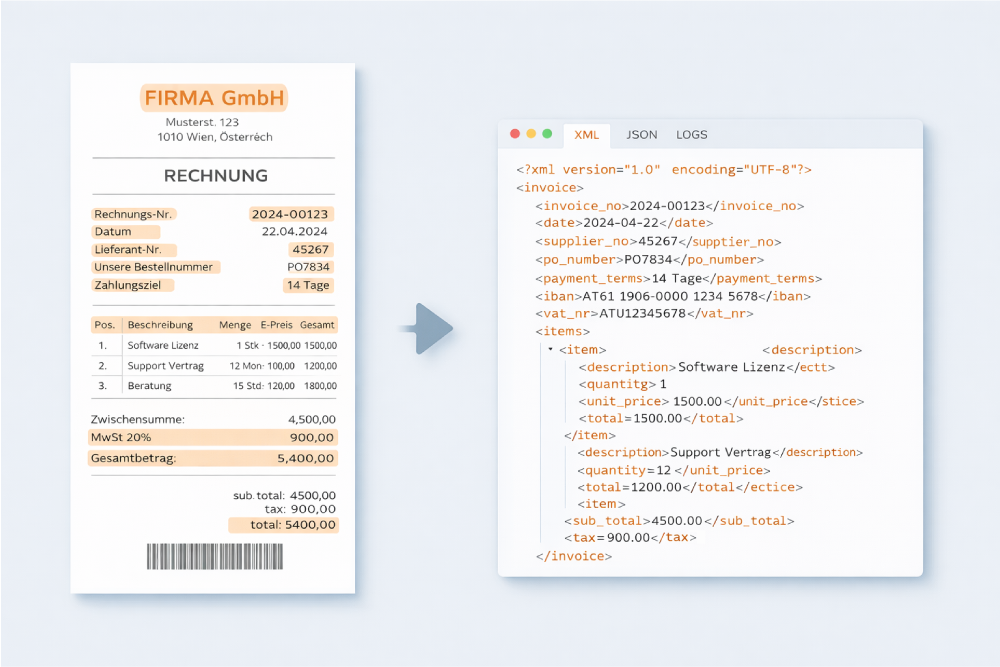

The most important difference between an e-invoice and a conventional PDF or paper invoice is the data format. According to the E-Invoice Regulation (E-Rech-V), which came into force in the B2B sector from January 2025, e-invoices must meet the requirements of the international standard EN16931. This means that only invoices issued in a structured electronic format (e.g. XML, UBL, EDIFACT) are considered e-invoices. Electronically issued invoices that do not contain a structured data set, such as PDF or image files, are therefore no longer permitted. Specially developed formats that do not comply with the official standards are also not normally permitted.

The structured format of e-invoices enables automated electronic data processing, which is associated with high cost and time savings in the long term.

Optimizing Costs and Workload Through E-Invoicing

The structured format of e-invoices enables automated digital invoice processing, which leads to significant cost and time savings in the long term.

You can save a considerable amount of money on both outgoing and incoming invoices. For example, the costs for printing, enveloping and sending invoices are eliminated for outgoing invoices. Your employees’ workload is also reduced as invoices are issued and archived automatically. When receiving invoices, you save on process costs, as processes such as processing, checking and archiving the invoice are handled automatically.

Thanks to the automated and electronic processing of these workflows, you save not only money but also time. Since less space is required for archiving invoices (folders, rooms, buildings, etc.), your employees no longer have to spend time searching for invoices. Processes such as handling complaints, monitoring incoming invoices, sending out reminders, and retrieving specific invoices during a tax audit can also be completed more quickly thanks to automated processing.

Formats for the E-Invoice

The two most commonly used standards for electronic invoices in Germany are XRechnung and ZUGFeRD. The EDI format, which has been in use for several decades, can also still be used for the time being.

EDI Format

EDI (Electronic Data Interchange) is a standardized format for the electronic exchange of structured business documents—such as invoices, purchase orders, or delivery notes—directly between companies’ IT systems. The transfer takes place fully automatically, without any manual intervention.

However, as EDI invoices do not always meet the requirements of the EN16931 standard, it is not yet clear whether this format can continue to be used after 2027.

XRechnung

The XRechnung is a pure XML file that contains all relevant invoice information. XRechnung has already established itself as the standard for exchanging invoices with public clients in Germany. It can only be read by machines and only be read by humans after conversion or with appropriate training.

ZUGFeRD

ZUGFeRD (“Zentraler User Guide des Forums elektronische Rechnung Deutschland”) is a standard for electronic invoices developed in Germany. ZUGFeRD combines structured electronic data (XML) with the visual representation in the form of a PDF/A-3 document. By combining these two file formats, the invoice can be read by humans (PDF) as well as read by machines and processed automatically.

The Most Important Legal and Organizational Requirements for Electronic Invoicing

By switching to an electronic invoice format, there are some important requirements that you should bear in mind when making the switch. The most important guidelines for e-invoices are

- Section 14 of the German VAT Act

- EU Directive 2014/55/EU and

- GoBD: the Principles for the Proper Keeping and Storage of Books, Records and Documents in Electronic Form and for Data Access

Tax Law Requirements for an (Electronic) Invoice

Every invoice, whether electronic or in paper form, must meet three requirements according to the UStG:

(1) Authenticity of origin: the identity of the invoice issuer must be clearly ensured

(2) Integrity of the content: Proof that the required tax information has not been changed after receipt of the invoice.

(3) Legibility: An invoice is considered legible if it can be read by humans. This is particularly important for formats such as XRechnung, as these can only be read by machines in their original form and must therefore first be converted. Readability must be guaranteed during the retention period stipulated by tax law (since 2025: 8 years).

In addition, the recipients of your electronic invoice must agree to the transmission procedure. You can obtain this consent explicitly, through prior or subsequent communication. However, consent is also deemed to have been granted if the invoice recipient pays the invoice without objection.

Control Procedure

Your company must have an internal control procedure in place to be able to prove the authenticity of the origin and the integrity of the content of the invoice. The control procedure must provide a reliable audit trail that establishes a traceable link between the invoice received and the service provided.

Since there are no legal requirements for the type of control procedure, this can be determined individually by the entrepreneur. In order to avoid media disruptions, it is advantageous to carry out this control procedure electronically. Since such a procedure must also be carried out for paper invoices, in most cases it is not necessary to introduce a new control procedure when switching to an e-invoicing system.

Data Storage and Web Download

In order to prove receipt of the invoice, the emails or other relevant data should be saved. If you use a document management system (DMS), electronic documents are automatically time-stamped, which allows you to prove receipt of the invoice – but you should still not delete the corresponding emails, as they often contain important additional information that could be relevant for a tax audit.

Important: Invoice receipt must also be documented if an invoice is downloaded online via a web download.

Electronic Archiving

Just like paper invoices, e-invoices must also be properly archived. Since 2025, they must be retained for at least eight years (BEG IV—previously ten years), and in Austria for seven years, in an unaltered and legible form for potential audits. The authenticity of their origin, integrity of their content and legibility must be guaranteed throughout the entire retention period. The necessary programs must therefore always be available, especially for the legibility of e-invoices.

When archiving, the original condition of the invoices must be preserved and verifiable. The most important regulations to be followed are Section 14 of the German VAT Act (UStG), Sections 146, 147 and 200 of the German Fiscal Code (Abgabenordnung) and the Principles for the Proper Keeping and Storage of Books, Records and Documents in Electronic Form and for Data Access (GoBD).

What Mandatory Information is Required for an E-Invoice?

To be recognized for tax purposes, invoices must comply with the provisions of the Value-Added Tax Act. The same requirements apply to electronic invoices as to paper invoices. However, the E-Invoice Regulation (E-Rech-V) specifies additional requirements that must be included in the e-invoice.

According to Section 14 of the German Value Added Tax Act (UStG), every invoice must contain the following information, among others:

- the full name and address of the service provider(s)

- the full name and address of the service recipient(s)

- the tax number or VAT identification number of the service provider(s)

- the invoice date

- a consecutive invoice number

- description and quantity of the products supplied or the service provided

- the invoice amount

- tax rate and tax amount, or a reference to any tax exemption

In addition to these VAT-related invoice components, Section 5 of the E-Rech-V stipulates that e-invoices must also include the following mandatory information:

- a “Leitweg-ID” – identification number

- bank details of the invoice issuer(s)

- terms of payment

- De-Mail or e-mail address of the invoice issuer(s)

Introducing Electronic Invoicing: Step by Step

When introducing e-invoicing in your company, there are a few prerequisites that you need to consider. First of all, your system must be prepared for processing e-invoices.

Note on outgoing invoices: Follow the steps mentioned above when creating and processing outgoing invoices as well. Create separate folders to keep the process organized.

E-Invoice Checklist: Some Questions You Should Ask Yourself During the Transition

When switching to e-invoicing, there are several technical and organizational requirements that must be met. The following checklist will help you keep track of all the important steps.

- Does your internal process hold up as an audit trail during a sales tax audit?

- Do you have your customers’ consent for electronic invoicing?

- Has a data format been selected?

- Can your system receive, read, and process the selected data format?

- Do you need additional software, and is your system’s storage capacity sufficient?

- Are adjustments to your audit trail necessary?

- Is your current hardware powerful enough for processing and archiving?

- If you handle your accounting through a tax advisor: Discuss the process for receiving electronic invoices and clarify any additional requirements.

Frequently Asked Questions About Electronic Invoices

Do You Have Any Questions For Us?

We will be happy to consult you during a short, non-binding online appointment!