Business Travel: Everything Employers Need to Know

Veröffentlicht am 01.07.2026

Lesedauer: 16 min

Contents

- What Counts as a Business Trip? Definition and Cases

- Travel Time on Business Trips: Active and Passive Travel Time

- Travel Expenses for Business Trips: Daily Allowance, Mileage Allowance and More

- How free-com Supports Travel and Expense Accounting

- Digital Business Trip Requests Before the Trip

- Capture Receipts Digitally on the Go

- Prepare Travel Expenses and Expenses Automatically

- Manage Approval Processes Transparently

- Improve Compliance and Travel Policy Adherence

- Integration Into Financial Accounting and ERP

- Frequently Asked Questions About Business Trips

Inhalt

- What Counts as a Business Trip? Definition and Cases

- Travel Time on Business Trips: Active and Passive Travel Time

- Travel Expenses for Business Trips: Daily Allowance, Mileage Allowance and More

- How free-com Supports Travel and Expense Accounting

- Digital Business Trip Requests Before the Trip

- Capture Receipts Digitally on the Go

- Prepare Travel Expenses and Expenses Automatically

- Manage Approval Processes Transparently

- Improve Compliance and Travel Policy Adherence

- Integration Into Financial Accounting and ERP

- Frequently Asked Questions About Business Trips

Business trips are often a fixed part of everyday business life. Whether for maintaining customer relationships, attending trade fairs, conducting contract negotiations or coordinating projects across locations, there are many business reasons why employees may need to work away from their usual place of work. If you send your employees on a business trip for this purpose, you as the employer are bound by a number of legal requirements. The following article provides a structured overview of the key obligations and regulations you need to observe.

What Counts as a Business Trip? Definition and Cases

A business trip generally occurs when employees leave their usual place of work on behalf of the employer to perform a professional task at another location. In Austria, tax law distinguishes in particular between the 1st case, the 2nd case and business trips based on wage-setting regulations. In Germany, the term commonly used is “beruflich veranlasste Auswärtstätigkeit” – a professionally required external activity, meaning work performed away from the employee’s home and first place of work.

It is important to distinguish this from ordinary work activity. Someone who regularly travels from customer to customer within their usual area of work is not automatically on a business trip. The decisive factors are the assignment, purpose, location, duration and the applicable employment law or collective agreement provisions.

Note: This article provides a general overview. It does not constitute tax or legal advice. For specific questions, please contact your tax advisor or an employment law expert.

Business Trip: 1st Case (Austria)

The 1st case applies in Austria when employees leave their place of work on behalf of the employer to work at another location, but daily return to their place of residence is reasonable. Typical examples are appointments in the nearby area, such as a customer meeting, a meeting at another branch office or training within reachable distance.

Example: An employee normally works in an office in Vienna and travels to a customer in St. Pölten for a half-day project meeting. She returns home on the same day. This may qualify as a business trip under the 1st case. For the tax-free treatment of daily allowances, however, it is important whether a new center of activity is established at the assignment location. If work is carried out regularly at the same assignment location, specific time limits apply.

Business Trip: 2nd Case (Austria)

The 2nd case applies to business trips where employees work so far away from their usual place of work or place of residence that daily return is not reasonable. In Austria, return is considered unreasonable in any case from a distance of 120 kilometers.

Example: An employee from Vienna is sent to Innsbruck for a project lasting several weeks. Daily return would not be practical. In this case, daily allowances can be granted tax-free at one and the same location for a limited period. From the seventh month at the same location, paid daily allowances generally become taxable. If the place of work changes, the period starts again.

Business Trip Under Applicable Remuneration Regulations (Austria)

If a wage-setting regulation, such as a collective agreement, works agreement or statutory provision, contains its own definition of a business trip, this definition takes priority. This third case is particularly relevant in practice for industries with a high proportion of field service or assembly work.

Typical activities covered include field service and customer visits, driving activities such as delivery services and transport, construction site and assembly work, and temporary agency work.

Example: A fitter employed by an electrical company who travels to different construction sites in several municipalities each week is typically subject to collective agreement business trip rules. Daily allowances of up to a maximum of 30 euros per day can be paid tax-free without a time limit, as long as the collective agreement requirements are met.

Germany: In German income tax law, the term “external activity” is used when employees temporarily work outside their home and their first place of work. The tax rules for meal allowances and travel expenses are set out in Section 9 of the German Income Tax Act (EStG).

Travel Time on Business Trips: Active and Passive Travel Time

Employers who send employees on business trips also need to deal with the question: what actually counts as working time, and what does not?

The basic rule is: travel time is always working time. Whether it counts as normal working time or must be compensated as overtime depends on the applicable collective agreement, a works agreement or the individual employment contract.

Active Travel Time

Active travel time occurs when employees perform work during the journey. This applies to driving a company vehicle as much as to preparing presentations during a train journey, conducting customer calls or studying files on a laptop.

Active travel time is always full working time and must therefore be remunerated with full pay. An agreement on lower remuneration or unpaid work is not permitted. If active travel time occurs outside normal working hours, overtime arises, including the corresponding supplements.

Passive Travel Time

Passive travel time occurs when employees travel on the employer’s instruction but do not perform any work, for example as a passenger on a train, bus or airplane.

Passive travel time also counts as working time and must be remunerated. Unlike active travel time, however, lower remuneration may be agreed here, provided this is expressly stipulated in the collective agreement, a works agreement or the employment contract. If no such agreement exists, passive travel time must be compensated in full.

Special rule: passive travel time may cause daily working time to exceed 12 hours and weekly working time to exceed 60 hours. However, this only applies if the journey is made by public transport or as a passenger in a car and no work is performed during the journey. Collective agreements often contain specific rules on this, which must be checked in each individual case.

Practical Note for Employers: Since the rules vary considerably depending on the applicable collective agreement, a clear contractual agreement on the compensation of travel times is recommended. Without such a rule, the entire travel time must be remunerated with full pay, which can lead to unexpected additional costs.

Travel Expenses for Business Trips: Daily Allowance, Mileage Allowance and More

If your employees incur costs during a business trip, you as the employer are generally obliged to reimburse them.

The most important travel expenses include:

- Travel costs, such as train, flight, taxi, rental car or mileage allowance

- Additional meal expenses in the form of daily allowances or meal allowances

- Overnight costs, such as hotel costs or overnight allowances

- Incidental travel expenses, such as parking fees, tolls or necessary telephone costs

- Other documented expenses if they are directly related to the business trip

The specific rates and legal bases differ by country: while collective agreement provisions are decisive in Austria, Germany is guided by the tax allowances under the Income Tax Act. Correct accounting protects against legal risks and secures tax benefits.

Daily Allowance for Business Trips

The daily allowance, referred to in Germany as a meal allowance or additional meal expense allowance, is used to compensate employees on a flat-rate basis for additional costs incurred due to meals away from home. It can be paid without individual receipts.

Austria

Daily allowances can be granted free of wage tax up to a certain amount. The tax-free maximum amount is 30 euros per day. For business trips lasting less than 12 hours but more than 3 hours, 2.50 euros per hour are tax-free. The tax-free daily allowance is calculated according to the 24-hour rule. Settlement by calendar day is alternatively possible if an employment law provision or corresponding employer practice provides for it.

A reduction of the tax-free daily allowance is required if the employer pays for meals: each business meal reduces the tax-free amount by 15 euros. If two or more paid meals are provided, the tax-free portion is eliminated completely.

The exact amounts to which employees are entitled under employment law depend on the applicable collective agreement. A distinction must always be made between the employment law entitlement, meaning what is owed, and the tax treatment, meaning what is tax-free.

For international business trips, separate country-specific flat rates published by the Austrian Federal Ministry of Finance apply.

Germany

In Germany, the meal allowance is governed by Section 9 (4a) EStG. For domestic business trips, the following tax-free rates remain unchanged for 2025 and 2026:

- 14 euros for an absence of more than 8 hours and less than 24 hours, as well as for arrival and departure days on multi-day business trips

- 28 euros for an absence of at least 24 hours

No meal allowance is available for external activities with an absence of less than 8 hours. For international business trips, the German Federal Ministry of Finance publishes an annual country overview with country-specific flat rates. For 2026, these were updated by BMF letter dated December 5, 2025.

If the employer provides meals, the allowances must be reduced accordingly: 20 percent for breakfast and 40 percent each for lunch or dinner.

The calculation methods differ for one-day and multi-day business trips. For multi-day trips, the arrival day, full travel days and departure day must be considered separately.

Important for employers: employment law entitlement and tax-free treatment are not the same thing. A collective agreement may provide for higher amounts, but only the permitted maximum amount is tax-free. The remainder may be taxable.

Mileage Allowance for Business Trips

If employees use their private vehicle for a business trip, they are entitled to reimbursement of the resulting costs. The mileage allowance is a flat rate that covers all vehicle costs, including fuel, wear and tear, insurance and maintenance.

Austria

A new mileage allowance regulation has applied in Austria since January 1, 2025 (BGBl II Nr. 289/2024). From July 1, 2025, the following tax-free rates apply:

- Passenger car and estate car: 0.50 euros per kilometer

- Motorcycle: 0.25 euros per kilometer

- Bicycle: 0.25 euros per kilometer (up to 3,000 km per year)

- Passenger transport: additional 0.15 euros per kilometer and passenger carried (documentation of names required)

The upper limit for tax-free mileage allowance is 30,000 kilometers per assessment year. For proof, a logbook or sufficiently detailed travel expense report is advisable. In particular, the date, starting and destination point, purpose of the trip, odometer reading and kilometers driven are required. The amounts stated are the maximum tax-free amounts that can be paid. The employee’s employment law entitlement may differ depending on the collective agreement.

For international business trips, separate country-specific flat rates published by the Austrian Federal Ministry of Finance apply.

Germany

In Germany, the tax-free mileage allowance for business trips with a private passenger car remains unchanged at 0.30 euros per kilometer in 2025 and 2026. For motorcycles and mopeds, a rate of 0.20 euros per kilometer applies. Employers can reimburse this amount tax-free, and there is no need for extensive individual receipt documentation. If the employer does not exceed the flat rate, employees can claim the difference as income-related expenses in their tax return.

Note: If a company car is used, the option to claim the mileage allowance does not apply.

Overnight Allowance and Travel Expense Allowance

Multi-day business trips involve accommodation costs. Here, too, there are clear rules for tax treatment.

Austria

The overnight allowance can only remain tax-free if an overnight stay actually takes place. In principle, the overnight stay must be documented. However, if the distance between the assignment location and the place of residence is at least 120 kilometers, the employer’s obligation to verify this no longer applies.

Two options are available:

- Without receipt: flat rate of 17 euros per night (including breakfast), tax-free

- With receipt: the actual overnight and breakfast costs can be reimbursed in full by the employer and remain tax-free

For international business trips, country-specific flat rates also published by the Austrian Federal Ministry of Finance apply.

Germany

Accommodation costs can be reimbursed tax-free by the employer in the actually documented amount, provided a receipt is submitted. Without a receipt, only an overnight allowance of 20 euros is available. For international overnight stays, the German Federal Ministry of Finance also publishes country-specific flat rates.

Correct accounting for overnight costs requires a clear distinction between the flat-rate allowance and reimbursement based on actual receipts, and the consistent application of the relevant procedure.

Would you like to learn more about travel expense accounting? Then continue reading our guide to travel expense accounting.

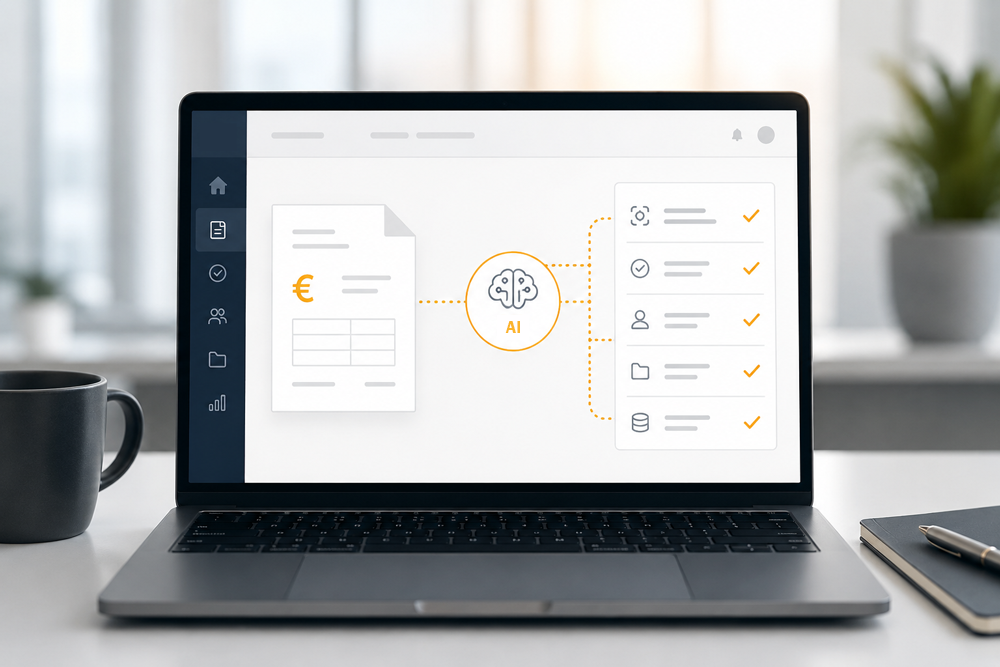

How free-com Supports Travel and Expense Accounting

In many companies, the process for travel and expense accounting is still paper-based and chaotic: collecting receipts, searching for photos in emails, filling out Excel files, looking up daily allowances, calculating mileage allowances, reminding managers, answering queries, submitting missing receipts. In short: a lot of work.

free-com helps companies handle travel requests, travel expenses and other expenses digitally and transparently. The entire process can be mapped centrally, from planning and receipt capture to approval and transfer to downstream systems.

Additional Benefits:

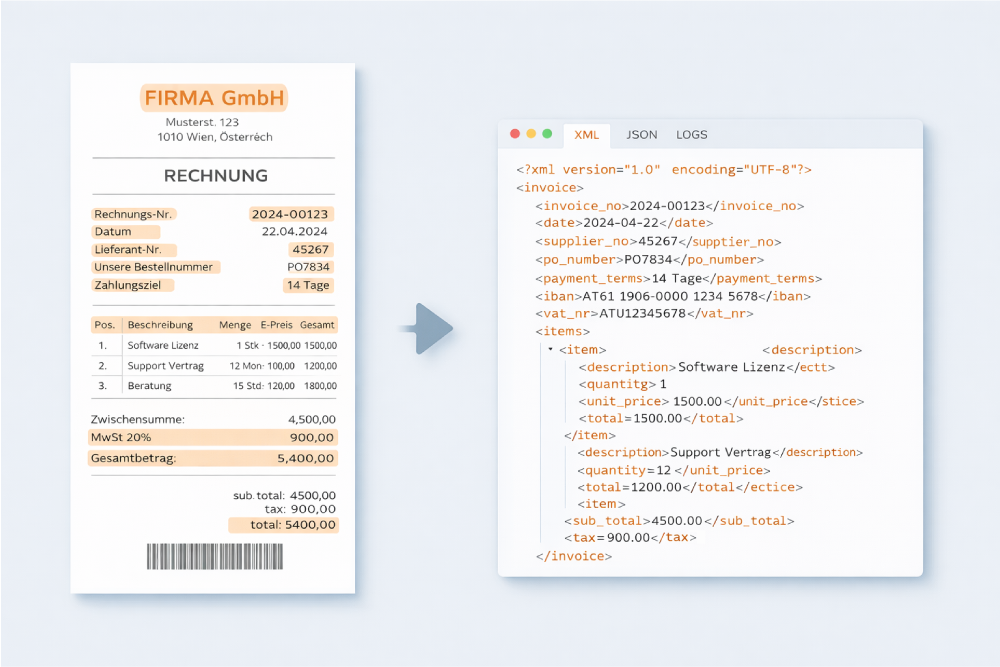

Capture Without Media Breaks

Employees capture receipts, kilometers and daily allowances directly via an intuitive interface – mobile or on desktop. No paper chaos, no lost receipts.

Rule-Based Calculation

Valid flat rates for daily allowance, mileage allowance and overnight costs for Austria and Germany are stored and applied automatically. This reduces errors and saves time during review.

Digital Approval Process

Expense reports pass through structured approval workflows. Managers review and approve directly in the system. The status is transparent at all times.

Seamless Integration

Approved expense reports are transferred directly to common ERP and accounting systems. No duplicate entry, no manual rework.

Audit-Proof Archiving

All receipts and expense reports are stored on EU servers in compliance with the GDPR and archived in an audit-proof manner. This means you are prepared for tax audits at any time.

Transparency and Traceability

Who submitted what, and when? Which receipts are available? Which expense reports are still open? The system gives you a complete overview at all times.

Do You Have Any Questions For Us?

We will be happy to advise you in a short, non-binding online appointment!